The fixed income outlook for ETF investors

- 15 November 2024 (5 min read)

KEY POINTS

The last 18 months have, overall, seen fixed income offer ETF investors positive total returns with companies weathering macro uncertainty and yields still at attractive levels. With Donald Trump soon to move back into the White House, central banks beginning their rate cut process and macro data remaining mixed, what is the outlook for fixed income ETFs?

The election of President Trump in the US was followed by the expected market reaction of higher Treasury bond yields and a stronger dollar. This was due to the market’s belief that Trump’s presumed policies will be fiscally expansionary and inflationary which may prevent the Federal Reserve (Fed) from cutting interest rates to the extent previously expected. Growth is arguably above trend, inflation is still above target, and so the Fed might need to keep rates on the tighter side of neutral for longer. Nevertheless, as seen with the 25 basis points (‘bps’) cut on 7 November, the Fed is continuing with its rate easing which may limit the extent to which yields will rise.

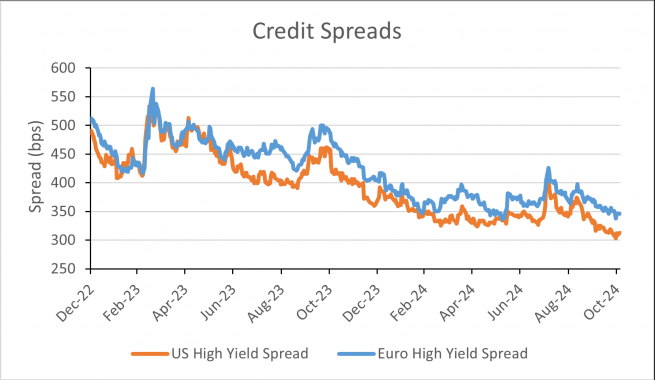

Credit spreads remain tight compared to historic standards, as seen below, reflecting an environment where the underlying economy is reasonably strong, which has brought down the credit spread premium.

Overall, credit has continued to outperform, particularly further down the credit curve. On a year-to-date (YTD) basis, the US high yield (HY) market has continued to outperform other fixed income markets, providing a return to investors of 8.03% compared to 5.76% for US investment grade and 3.02% for 10-year US Treasuries.1

While credit spreads are tight, we expect US high yield to benefit, at least in the short term, from Trump’s expected tariffs which are aimed at bolstering domestic growth and therefore should also keep spreads contained and default rates low.

On the other side of the Atlantic, the European Central Bank (ECB) has partly achieved its objective to reduce inflation. The ECB now also has options if it needs to react in the event of a downturn in the economy. This should be positive for euro credit going forward.

At the moment, euro credit all-in yields at current levels are well above the 10-year average, even though the fundamentals of some of these issuers are very solid and resilient. However, this is primarily due to higher government bond rates, as opposed to credit spreads, where the situation is a little different. This is because, like in the US, we have seen very significant tightening of these credit spreads over the last twelve or so months.

From a technical perspective, it has been an important year with a huge appetite from the market. We are seeing new issues that are subscribed sometimes four or five times the amount issued and we expect this supply/demand imbalance to remain in place for the months ahead.

Euro high yield, in particular, has experienced strong performance thanks to favourable company fundamentals. Alongside this, the default rate, while high compared to the pre-COVID era of quantitative easing and cheap re-financing , remains at manageable levels today, helping total returns.

Across sectors, financials continue to look an attractive sector with key risks such as non-performing loans still at low levels. While real estate issuers, who tend to be quite leveraged and so have been out of favour since rates began to rise in 2022, are now able to issue across all seniorities as rates fall. So, whether it is senior debt, subordinated debt, perpetual debt or the famous AT1, we believe it is a very dynamic market.

Further afield

For ETF investors looking for greater diversification across their fixed income portfolio, emerging market (EM) debt may worth considering. There has not been a lot of focus on emerging markets over 2024 for reasons such as China’s property crisis and concerns over far tighter US monetary policy which has bolstered the attraction of cash.

However, better market returns, an improving economic backdrop and the prospect of lower US interest rates suggest now might be the time to reassess their potential. Indeed, a soft-landing scenario for the US economy remains our base case however with the Trump win this could see a revision of the timing and frequency of rate cuts. This may influence other central banks’ policy cycles and reduce tailwinds for the emerging market debt. At the moment, better EM GDP growth is expected given the strong US economy and Chinese stimulus, especially if Chinese policies move to the top of expectations.

Across EM Sovereigns we are seeing a strong upward trend of upgrades versus downgrades for EM sovereigns we have seen in the second half of 2024. For EM corporates, earnings growth YTD has been healthy and revised higher for 2024 as pockets of disinflation has helped temper input costs.

EM HY companies generally have liquidity buffers in excess of their short-term obligations and with China real estate largely removed from the index, we expect the default rate to be significantly lower in 2024 versus last two years.

Variety is the spice of life

Even as rates begin to fall, we are not in the zero-rate environment that haunted the bond market for so long. However, with higher yields comes volatility. Fortunately for ETF investors, there has never been as much choice for fixed income investing as there is today. With both active and passive investment approaches on offer, ETF investors have options across different geographies and themes to meet their needs.

- U291cmNlOiBBWEEgSU0sIElDRSBCb2ZBIGFzIG9mIDMwdGggU2VwdGVtYmVyIDIwMjQ=

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.