China – Eyes on trade fragmentation

KEY POINTS

Tariffs would threaten economy

The upcoming US election could significantly affect China’s economy, primarily through trade fragmentation. Both presidential candidates have discussed tariffs, though Donald Trump has threatened much larger increases than Kamala Harris – up to 60%. Exports have been a crucial driver of China’s economic growth, especially considering its several domestic challenges. The possible increase in US tariffs on Chinese goods could exert considerable pressure on China, subsequently dampening overall economic growth. Moreover, further disruptions in US-China trade relations could erode investor confidence. In recent years, China has become less attractive to foreign investors due to increased government intervention. Additional tariff hikes would heighten uncertainties, threatening to further reduce foreign investment in China.

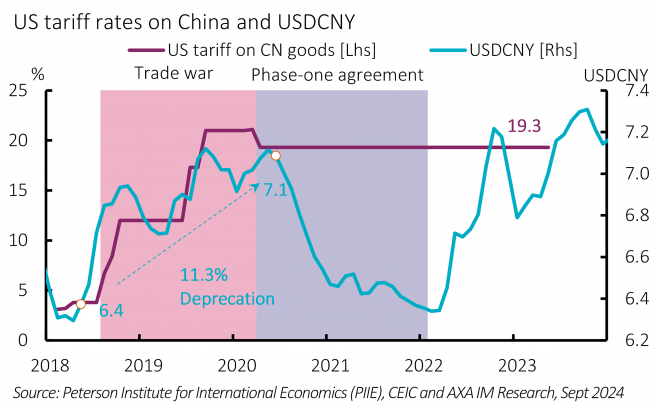

In Trump’s first term average US tariffs on Chinese goods surged from around 4% in early 2015 to 21% by late 2019, settling at 19.3% following the Phase-One agreement in early 2020. As a result, Chinese exports to the US dropped sharply in 2019, partially recovering in 2020. On average, exports to the US declined by 3% annually between 2018 and 2020, partially mitigated by the yuan’s depreciation. The yuan fell by 11.3%, from 6.3 to 7.1 against the US dollar (Exhibit 5), as the People’s Bank of China allowed devaluation in line with market forces.

If a blanket tariff of 60% on Chinese goods were imposed, based on 2023 export values, Chinese exporters would face over $200bn additional tariffs annually, equating to 1.2% of China’s GDP. As in the previous trade dispute, such a tariff increase would likely lead to a natural appreciation of the US dollar (depreciation of the yuan), which could mitigate some pressures. Nevertheless, the impact could still be significant and poses two major challenges.

A persistent negative output gap in China’s economy has led to a low-inflation environment, increasing the risk of entering a debt-deflation loop. A decline in external demand due to higher tariffs would slow growth, exacerbate this output gap and reinforce disinflationary pressures, including an increase in unemployment, particularly in export-dependent sectors, further weakening the labour market and dampening consumer confidence further.

Higher US tariffs could also trigger capital flight from China. The yuan is already weak due to a strong US dollar and China’s economic slowdown. Further tariff hikes could push the currency to new lows with significant yuan depreciation possibly triggering capital flight, particularly if combined with slower economic growth, stock market declines and worsening risk perceptions. Both domestic and international investors may seek more stable/profitable opportunities elsewhere, particularly if they anticipate prolonged economic challenges. The scale and immediacy of capital flight would also depend on the severity of any tariff increases, the broader economic environment, and the Chinese government’s response to these pressures, but could further destabilise China’s economy.

Despite these challenges, the impact of tariff increases could be less pronounced than in 2018. China has increasingly diversified its exports away from the US and strategically enhanced a deeper integration into key global supply chains – such as semiconductors, batteries and solar panels – which may offer some protection against future trade disruptions. However, these new supply connections could be more vulnerable to sanctions, with third parties encouraged to observe – which US Democrats have made more use of – than pure tariffs, which Trump favours.

The US election therefore poses a risk to the fragile outlook for China’s economy whatever the outcome. However, the suggested scale of tariff increases proposed by Trump pose the biggest risks. Proactive and adaptive policy responses will likely be crucial in navigating these uncertainties as well as delicacy in handling other geopolitical developments.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.