US reaction: Inflation slowing in line, but nothing weaker

- 14 August 2024 (3 min read)

KEY POINTS

Headline inflation in July slowed to 2.9% - the first time it has been below 3% since March 2021. This was modestly below expectations, although with the monthly rise coming in at 0.155% vs the 0.2% consensus expected, the miss was modest (2.92%). Perhaps more importantly, core inflation also came in at 0.165% (versus a 0.2% consensus) and the annual rate slowed to 3.2%, in line with expectation, the lowest since April 2021.

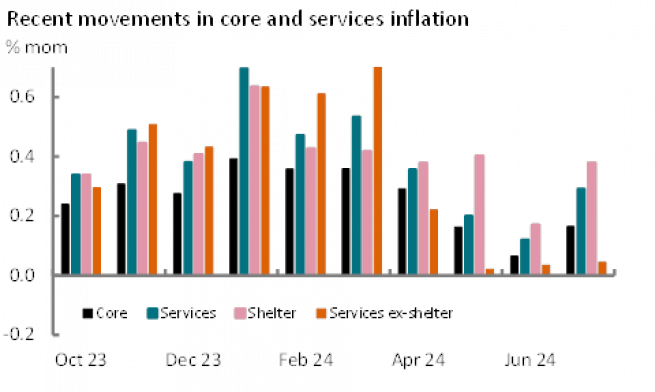

A breakdown of July’s inflation revealed several moving parts. Fuel prices continue to contribute to a lower headline rate. Annual motor fuel price inflation is -2.3%. Goods price disinflation persisted, with a monthly fall of 0.3% in July – the biggest fall since January – and the annual rate remaining at -0.4%. This was driven by further steep declines in used car prices – down 2.3% on the month – and a fall in clothing prices. Both of these developments are consistent with an ongoing softening in consumer spending, although household furnishing completed their second month of solid gains following sharp contractions in April and May. The Fed’s focus will continue to fall on services inflation, which remains elevated at 4.9% - albeit a joint 2½ year low. Overall these rose by 0.3% on the month, firmer than the previous two months’ readings, but still below the average pace of H2 2023 and far below the pace set in Q1 this year. Exhibit 1 below illustrates that this was dominated by firmer readings again in shelter. Shelter inflation rose by 0.38% on the month, with a small rise in owner equivalent rents (0.36% and still below every reading before last month), but rents on primary residences rose by 0.49%, the biggest increase in a year and a move that suggests a basic catch-up from last month’s weak reading, with rents now averaging around 0.4% since December (barring February). By contrast, ex-shelter services inflation remained soft, rising by just 0.04% on the month again, in turn reflecting softer price increases in medical care (-0.25%), transport and personal care.

In broad terms, today’s release can be seen as continuing to add to evidence that inflation is broadly in line with achieving the Fed’s target, consistent in our minds with a gradual removal of policy restriction over the coming quarters. However, the Fed’s – and broader market’s – focus has now shifted towards the labour market and a softer July report has reignited fears in markets of a sharper slowdown in activity ahead. In part, this should continue to reduce the emphasis on the monthly inflation reports as the Fed’s confidence of retaining anchored inflation expectations grows and its focus naturally shifts towards the outlook for inflation, not the outcome. That said, today’s report downplays some concerns that the Fed has overtightened policy – inflation looks likely to be coming down to around target rather than exhibiting signs of materially undershooting it. As such, we continue to view market expectations for 100bps of easing this year and another 100bp by this time next year as over-cooked. We expect the Fed to begin to gradual ease restrictive policy in September and forecast another cut in December. Beyond that outlook, we consider the outcome of November’s election as pivotal and beyond the honeymoon resurgence in Democrat fortunes under Vice President Kamala Harris’s candidacy, we still on balance expect to see Donald Trump return to the White House, something that we think could restrict the Fed’s ability to continue rate cuts in to next year.

Financial markets saw some reaction to a basically ‘in line’ outcome. Chances of a 50bps cut in September were scaled back by around 8ppt, now seen at a little over a one-third chance, but the market still almost fully prices 100bps of cuts by year-end. As such, 2-year US Treasury yields rose 4bps to 3.97% and 10-year 3bps to 3.86%. The dollar rose around 0.2% immediately after the release, but retraced all of those gains.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© AXA Investment Managers 2024. All rights reserved