Multi-Asset Investments Views: Guess Who’s Back?

- 02 December 2024 (5 min read)

Donald Trump is back, becoming the 47th US President in January. Historically, US presidential elections have had limited impact on financial markets. This time around however, and as in 2016, the massive divergence in policy agenda between the candidates saw some ‘Trump trades’ move back and forth in sync with polls. Once the result was confirmed, these Trump trades kept rising: US equities outperformed, the US dollar appreciated along with US Treasury yields, and US financials rose sharply on the prospects of deregulation in the next four years.

We reinforced our tactical positioning to follow the momentum in these trades, keeping an overweight exposure to the US dollar and favouring the US in our equity allocation with an emphasis on banks and domestic cyclicals. We maintain most of these positions, gaining some comfort given that US Treasury yields have edged lower, and marginally away from the ‘danger zone’ (above 4.5% in 10-year nominal yields and 2% for real rates). These levels of interest rates tend to hit equities via a multiple de-rating.

As the year ends, we examine our position in the current economic and market cycles. Our fundamental assessment is that we remain in the bull market initiated at the end of September 2022. Some 26 months later and with global equities around about 60% higher, this bull market is mature compared to historical precedents, although by no means extreme.1

Valuations are above their long-term average in some markets but the current richness is concentrated in a handful of specific, heavily-weighted US technology stocks. The 10 largest US companies offer a vivid example, trading at around 50 times their price-to-earnings ratio. However, many technology companies are transformative disrupters and a high valuation alone is not a reason to avoid them – but nonetheless, we find the rest of the US equity market more attractive. We anticipate a broadening of the US equity rally in 2025, especially as the gap in earnings growth between the so-called Magnificent 7 and the rest of the S&P 500 is estimated to narrow sharply from more than 30% in 2023 and 2024 to only 4% to 6% in 2025 and 2026.2

- KlNvdXJjZTogTVNDSSBXb3JsZCBJbmRleCBpbiBVU0QgQmxvb21iZXJnIGZyb20gMzAvMDkvMjAyMiB0byAyOS8xMS8yMDI0

- KipOdmlkaWEsIEFwcGxlLCBBbHBoYWJldCwgQW1hem9uLCBNaWNyb3NvZnQsIE1ldGEgUGxhdGZvcm1zLCBUZXNsYS4gU291cmNlOiBGYWN0c2V0IDE1LzExLzIwMjQ=

Entering a slowdown phase

A second Trump presidency is also a key to our positive view on US equities. An overweight on US over European equities was positively rewarded 80% of the time since the 2008-2009 global financial crisis due to a more favourable growth differential and investors’ sentiment.

The threat of US tariffs and China’s likely response through an exchange rate depreciation should add to the transatlantic divergence in growth and fiscal policy, once again to the detriment of Europe. Global and US equity markets have been in an expansion phase since the fourth quarter of 2023; with US growth above trend, technology and stocks described by the ‘momentum’ factor have outperformed.

Our Macroeconomic Research team expects that US real GDP will grow by about +2.3% in 2025 after +2.8% this year. We therefore expect equities to enter the slowdown phase of this cycle in 2025, which calls for an emphasis on quality and low-volatility stocks and the fading of the pure momentum factor. In Europe, we have most likely already entered this phase. In this context, we take a more defensive tilt towards the region, with an emphasis on interest-rate sensitive stocks. Similarly, we are constructive on duration via euro-denominated government bonds, as the European Central Bank’s tone now seems more aligned with the bloc’s fragile economic backdrop.

However, the divergence in past equity performances and in valuations would indicate it is not all a lost cause for Europe in 2025 – whether that is using trailing or forward earnings, currently sitting at unprecedented levels. Unfortunately, the same could have been said a year ago; and since then, US equities have outperformed their European counterparts by close to 20%.

Catalysts and risks

Mean-reversion, where asset prices and historical returns revert to their long-term averages, can take a long time to materialise in financial markets. Positive catalysts or upside surprises are conceivable: the end of the conflict in Ukraine; stronger stimulus in China; a more supportive German fiscal stance after the general elections in February. We are watching for a capitulation in investors’ sentiment and positioning.

Looking at potential risks, our worst-case risk scenario is a repeat of 2022 with interest rates rising to the point they would trigger a consolidation of equities due to a de-rating. We are confident that such an episode, if it were to occur, would be modest: the global economy is showing signs of a slowdown, more clearly so in China and Europe than in the US, and 10-year interest rates are already relatively elevated (compared to real potential growth and well-anchored inflation expectations).

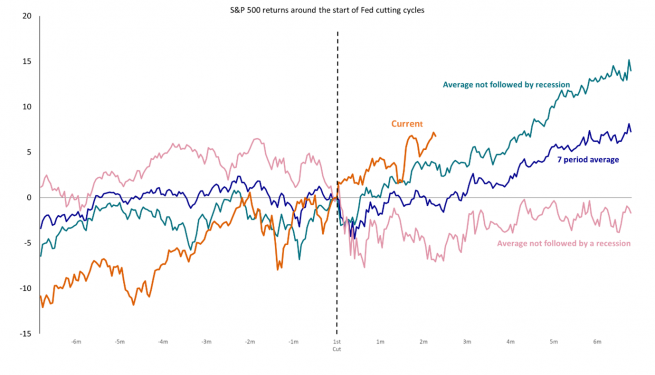

The most probable negative risk scenario remains the materialisation of a long-awaited US recession. In this scenario, German Bund and US Treasury yields would likely drop but equities would correct, due to significant downward revisions to earnings expectations. Overall, we remain confident that multi-asset strategies can offer the expected diversification and could potentially provide better risk-adjusted returns than single-asset strategies, whether in equities or bonds.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2024 AXA Investment Managers. All rights reserved

Images Source: Getty Images