Inflation reaction : ECB to cut rates in October

- 01 October 2024 (5 min read)

EMU | ||||||

Headline HICP (in % yoy) | Headline | Core | Germany | France | Italy | Spain |

AugustSeptember (AXA IM) | 2,2 | 2,8 | 2,0 | 2,2 | 1,2 | 2,4 |

| 1,7 | 2,7 | 1,7 | 1,7 | 0,6 | 1,6 | |

September (Refinitiv Consensus) | 2,0 | 2,8 | 1,9 | 2,0 | 1,0 | 1,9 |

September (Flash) | 1,8 | 2,7 | 1,8 | 1,5 | 0,8 | 1,7 |

Source: Eurostat, Bloomberg and AXA IM Research, October 2024

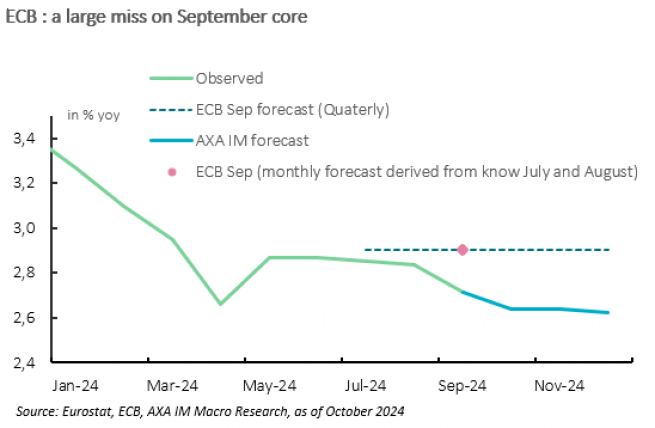

Euro area headline inflation dropped to 1.8% yoy in September (-0.4pt), slightly above our forecast but below consensus (2%). Energy deflation accounts for most of the deceleration (-6% yoy) but core inflation decelerated to 2.7% yoy (-0.1pt). It is in line with our forecast and below consensus (2.8%). But most importantly it is a large miss versus ECB September macroeconomic projections. The ECB had a core inflation averaging 2.9% in Q3, which implied a figure around 2.9% for September (Exhibit 2).

ECB to cut rates at its October meeting. Considering the persistent nature of today's inflation downside surprise on ECB's forecasts, as well as the October meeting market pricing (25bps cut priced with over 90% probability), we now expect the ECB to cut rates by 25bps at its October meeting, reflecting their data-dependence and meeting-by-meeting approach. We will review our rate expectations beyond October and publish a revised path by the end of this week.

Faster core disinflation

EMU services inflation decelerated to 4.0% from 4.1% in August but the decline is less important than initially thought. We suspect French large decline in CPI services inflation (from 3% to 2.5%) has been less important through harmonised measure, while services inflation continue to remain elevated in several countries. It can be Germany that may have stronger services inflation through harmonized measure (CPI services inflation came at 3.8% ,from 3.9%), but we suspect some stickiness in the Netherlands and Belgium. In Italy, HICP services inflation declined by 0.3pt to 3.1% yoy.

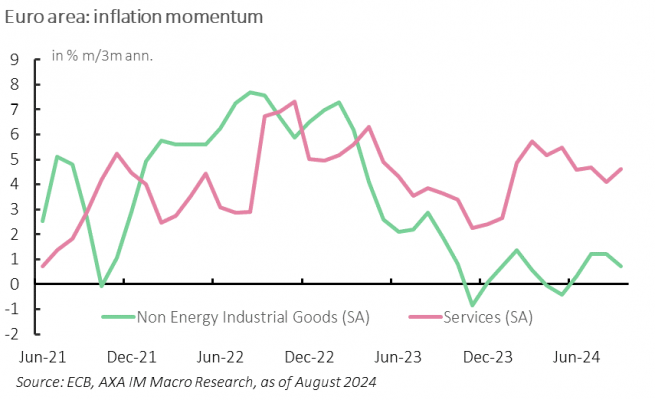

Consequently, the picture is a bit blurred. Services inflation stays elevated but disinflationary trend well entrenched. Monthly pace in September came at -1% (non-seasonally adjusted), much closer to last decade average while the ECB seasonally adjusted measure shows a small tick up (Exhibit 3).

All the more so as non-energy industrial goods (NEIG) inflation stayed muted at +0.4% yoy (flat from August). In several countries such as Italy and Spain, September is usually the month with some goods being repriced after the summer sales, but it seems weak demand weigh on the normalisation of prices (i.e Italian NEIG rose by 5.3% mom, a much lower level than the average in last decade that is closer to +8.5% excluding COVID period).

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© AXA Investment Managers 2024. All rights reserved