The Case for US investment grade credit in 2024

- 24 January 2024 (5 min read)

US corporates fundamentals remain attractive with solid balance sheets despite the environment of higher financing costs.

At a macro level, with the expectations that the Federal Reserve (‘the Fed’) will pause interest rate hikes, investors can potentially benefit from an attractive entry point and attractive yields.

1. Credit fundamentals remain robust

The US economy is likely to experience a soft landing in 2024 which, we believe could be supportive for sentiment and corporate spreads.

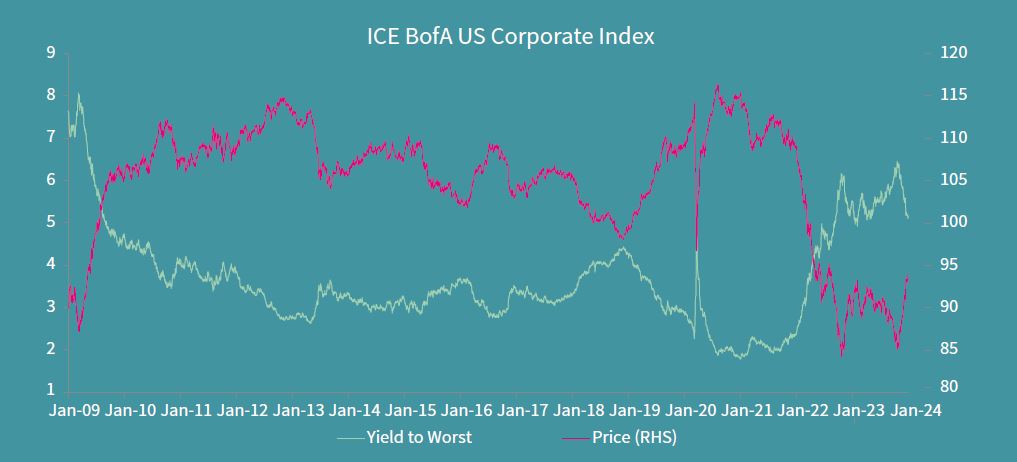

US IG yield and price evolution since 2009

Source: Bloomberg, AXA IM, from 1/2/2009 to 31/12/2023

► All-in credit yields for IG bonds are historically attractive having not reached these levels since 2009.

► IG credit may also offer attractive compensation for interest rate and credit risks.

2. Making size and liquidity matter

With a value of over US$8 trillion, the US credit universe accounts for roughly two-thirds of the global corporate market, and has several key features:

► Strong liquidity profile

► Diversified with an abundance of selection opportunities

► Positive technicals following a decline in issuance

3. Accessing short-to-intermediate duration strategies

An inverted US government bond curve creates comparable yields for short-to-intermediate vs full duration strategies without incremental interest rate and credit risks.

Key features of shorter duration bonds:

► An ability to boost liquidity via regular cashflows to the portfolio | ► A higher potential reinvestment rate by seizing opportunities when rates rise |

► A price closer to par for bonds nearer maturity versus longer duration bonds | ► Lower volatility in returns compared with the broader market |

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.