New disorder

- 21 February 2025 (3 min read)

The Trump Administration has become the key source of global geopolitical risk. It is disrupting the status quo. Profound political and economic consequences are possible. US exceptionalism is morphing into something less palatable. The big question is: will the rest of the world keep financing the US? Fractured relationships, adversarial trade policies, and a need to increase defence spending in Europe might disrupt capital flows. Valuations for US stocks and bonds could well be at risk.

Winds of change

By accident or design, US President Donald Trump is disrupting the global political and economic order. Alliances and institutions are under threat because of his pursuit of an America first agenda. We are seeing the US pull out of international institutions and agreements, which is threatening its relationship with the rest of the western alliance and also disrupting the global trading system. The disorder could have profound investment implications. Yet markets have been calm. The 10-year US Treasury yield has been in a 25-basis point (bp) range since the inauguration. The S&P 500 index has traded in a 200-point range (3.4%) and the dollar index is down just 2%. So far, the significant implications of the new Administration’s global approach have been met with a big fat “whatever” by markets.

Straight up

It is difficult to anticipate the impact of Trump 2.0. This may explain why markets have been muted. Having said that, there are signs that global investors may be shifting a little away from the US in their allocations. European markets have outperformed. The Euro Stoxx index has delivered a total return of close to 11% year-to-date, compared to 4.6% for the S&P 500. Emerging market and global high yield debt indices have performed much better than US investment grade credit and the Treasury index. Returns are positive across the board. It seems markets don’t believe the world order is about to be overturned. That may prove to be too sanguine a view.

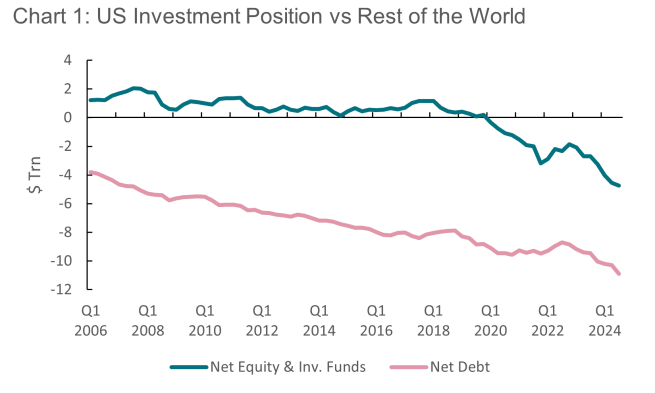

Rip it up

The US trade deficit is a source of frustration for President Trump. He appears to see it as a reflection of an unfair global trading system with other countries “ripping off the US”. Years of running trade deficits has made the US very indebted to the rest of the world. US Bureau of Economic Analysis (BEA) data shows the US had a net negative international investment position of almost $24trn as of the third quarter (Q3) of 2024 (see chart). The rest of the world has accumulated dollar assets as counterpart to the trade gap. Trump is railing against this state of affairs.

Reserve currency

My son recently bought me a book, Broken Money, by Lyn Alden. It is a critique of fiat currencies and an argument for Bitcoin becoming a technology-age successor to gold as a safe(r) store of value. I’m not convinced, even though I have a lot of sympathy with her analysis of the global monetary order. She and others would argue that fiat currency systems encourage growth in debt, unanchored monetary expansion and inflation that erodes the value of creditor assets (savings). Her description of the growth in the role of the dollar as the global reserve currency deserves some attention. Some of Trump’s frustrations are interlinked with the dollar reserve currency framework. The rise in the price of gold in recent weeks suggests some investors feel that this frustration might evolve into something more dramatic – although arguing for the US returning to the gold standard remains the purview of cranky conspiratory theorists on social media – for now.

The best

For numerous reasons – largely centred around the US’s political, economic and military strength in the latter part of the 20th century – the greenback became the pre-eminent global currency. Commodity and goods trades became priced in US dollars, and still are. There are strong reasons why the rest of the world should hold dollars – how else would we pay for oil? The quid pro quo for holding dollars as a reserve asset was increased access to the US economy for exporters. From the mid-1970s the US started to run trade deficits – first because of the oil shocks of that decade, then because of increased globalisation that saw Japan and then China increase their share of global manufacturing.

Dollars everywhere

Although the US has been strong in services trade, this has not been enough to offset the trade gap. The current account of the balance of payments has been in deficit for a long time. The counterpart to this is a capital account surplus. Exporters of commodities, industrial and consumer goods to the US receive dollars in payment. This led to the growth in dollar holdings in reserves at foreign central banks from the 1980s (e.g. Japanese exporter sends goods to the US, receives dollars in payment, exchanges dollars for Yen through the Japanese banking system, leaving the Bank of Japan with US dollars in reserves). The rest has been held by the private sector. Dollars have been held in cash or recycled into US Treasuries and other bonds, or into direct holdings in US real estate or companies, or into listed securities such as corporate equities and mutual funds. According to the Federal Reserve (Fed), foreigners own around $16trn of US corporate equities and $8.6trn of US Treasury securities.

Long US

While US Treasuries were traditionally the asset class that foreign central banks acquired, increasingly private capital flows into the US have gone into equities. BEA quarterly data shows that since 1991, 75% of the quarterly data points saw positive purchases of US equities by foreigners. In Q3 2024, foreigners purchased $230bn of stocks, mutual funds and US listed ETFs. The performance of the US market and the dollar has been very beneficial to these foreign investors. The stock market has been a key channel for funding the US trade deficit.

The premium afforded to the stock market of choice

Determining the causation between foreign inflows and the performance of US equities is impossible, but there is a correlation. The US has needed to attract foreign capital, the stock market has become an important channel for those investments and, arguably the cost of capital for US companies has been lower as a result. This may have contributed to higher profit margins and, importantly, the growth and persistence of a valuation premium in US stocks relative to the rest of the world.

What’s wrong hun?

What is it about this (some would say, vendor financing ponzi scheme) that President Trump doesn’t like? Americans own over 80% of the total market capitalisation of US corporate equities, so will have benefitted from stock market performance. America has many of the leading companies in the world which have leveraged foreign financial capital but also foreign intellectual capital flowing to the US (think technology firms). The dollar remains the reserve currency, despite periodic episodes of currency debasements and financial repression. The US government has been able to run and finance large deficits at interest rates that probably would not be realistic in other counties.

Trump doesn’t like the US being in debt, doesn’t like the fact that Americans buy more foreign made goods than foreigners buy America goods, and probably fears that large holders of US debt – China for example – might one day use that to their advantage.

Chaos

Tariffs are the weapon of choice to try and address the trade imbalance. Trump wants to make foreign goods more expensive in the hope that US consumers will buy less and/or that foreign producers will set up shop in the US rather than exporting output from abroad (thereby favouring US over foreign employment). Broad ranging tariffs have been threatened, even though only limited implementation has happened so far. We should not be in any doubt, however, that Trump wants a lower trade deficit even if that means upsetting traditional economic partners, disrupting supply chains and costs, and causing US inflation to go up.

Black swans

I said at the top that modelling all of this is difficult. There are lots of potential economic outcomes from a trade war. Think about this. If Trump is successful in bringing down the trade deficit, this means, by definition, lower capital inflows. If those inflows have helped sustain high valuation premiums for US equities, might lower net inflows undermine those valuations? What if the political risk premium attached to the US dollar increases? Might that mean less willingness in the rest of the world to hold US Treasuries and stocks. China has, for some years, been diversifying its foreign exchange holdings. A decade years ago, China accounted for 20% of foreign ownership of US Treasuries. Today it is less than 10%. A weaker dollar and higher US bond yields are potential tail risk outcomes if the US goes further down an adversarial route.

I attended a geopolitical risk presentation this week. The speaker argued that the US was the primary source of geopolitical risk today – it never has been before. We are in unchartered territory. Discussing potential outcomes for the Ukraine war is beyond the scope of this note but some are extremely unpalatable for those of us brought up in a world where security was based on the US being on our side. Given China’s recent challenge to Silicon Valley, the apparent side-stepping of Congress in policy making, and the new set of US foreign policy risks, might it possibly be time to rotate away from US markets and bring money closer to home? (And maybe hold some gold and/or Bitcoin?).

(Performance data/data sources: LSEG Workspace DataStream, Bloomberg, AXA IM, as of 20 February 2025, unless otherwise stated). Past performance should not be seen as a guide to future returns.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.