EM reaction: no respite (yet) in inflation pressures in Turkey

- 03 April 2024 (3 min read)

March headline inflation reached 68.5% year-on-year, core inflation reached 75.2%, from 67.1% and 72.9% respectively in February

On a month-on-month basis, consumer prices progressed by 3.2% which was below the 3.5% expected by the Reuters consensus. Still, inflation rate shows no signs of respite so far, in spite of the 4,150bp cumulative interest rates hike delivered by the Central Bank of Turkey (TCMB) since May 2023.

Inflation momentum points to higher inflation for some months to come

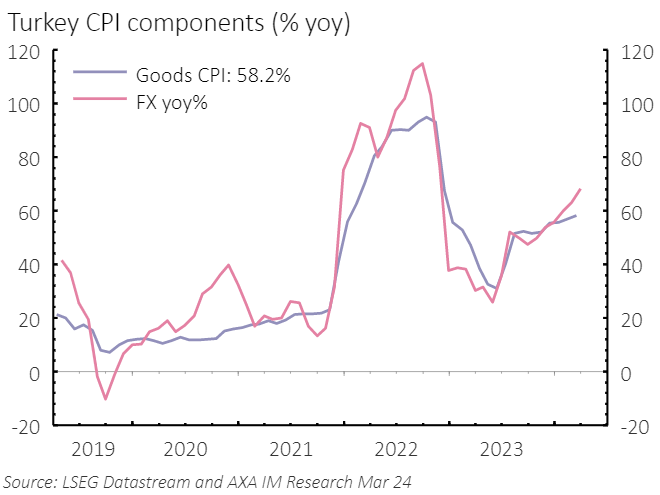

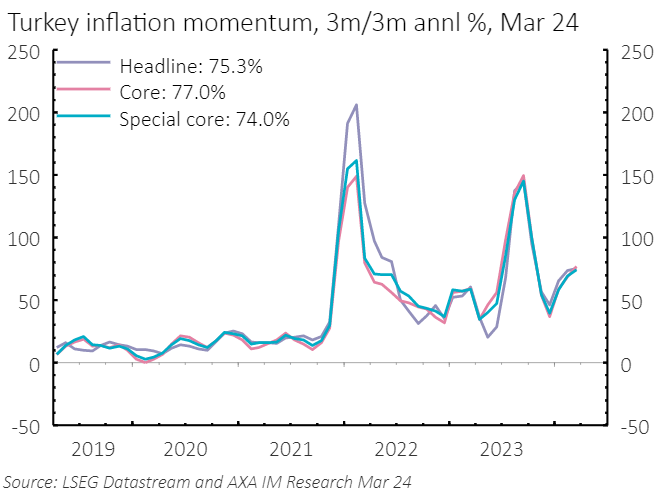

Food prices were helpful in March but clothing, transportation and housing prices all pushed inflation higher. In March, goods inflation run at 58.2% and remained under pressure given the past currency depreciation pass-through via imports. Services prices, in particular, which usually display more stickiness, have continued to post a strong increase (+4.2% month-on-month), annual inflation in the services sector accelerated thus further to 96.5%. On a 3-month/3-month annualized basis, core and special core inflation momentum is running around 74-77%.

Inflation expected to decline in the second half of the year

In its latest inflation report (February), the TCMB was expecting headline inflation to increase throughout the first half of 2024 and decline steadily as of the second half, to reach 36% at the end of 2024 and 14% at the end of 2025. March survey of expectations pointed to further de-anchoring of inflation expectations, at 44.2% for year-end, which in turn has contributed (alongside other factors) to the latest 500bp rate hike. We expect inflation to continue to accelerate at least until May-June, and start decelerating thereafter. The pace of deceleration will be intimately linked to the forcefulness of the fiscal policy tightening measures which should be implemented now that the local elections are out of the way. For now, we pencil in inflation closer to 45% year-end and we do not expect further rate hikes. The central bank retained quite a hawkish forward guidance: “Tight monetary stance will be maintained until a significant and sustained decline in the underlying trend of monthly inflation is observed, and inflation expectations converge to the projected forecast range. Monetary policy stance will be tightened in case a significant and persistent deterioration in inflation is foreseen.” We believe they will be inclined to keep a tight stance through the rest of the year and would only revert to rate cuts if inflation decelerates quicker than expected. For now, we expect policy rates unchanged at 50% by year-end.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© AXA Investment Managers 2024. All rights reserved